This article contains latest information about the Biden Administration’s plan to provide student debt relief to eligible borrowers. Find out important information about who’s eligible.

On Aug. 24, 2022, the Biden Administration announced a Student Debt Relief Plan that includes one-time student loan debt relief targeted to low- and middle-income families.

The U.S. Department of Education will provide up to $20,000 in debt relief to Federal Pell Grant recipients and up to $10,000 in debt relief to non-Pell Grant recipients. Borrowers with loans held by the U.S. Department of Education are eligible for this relief if their individual income is less than $125,000 (or $250,000 for households).

While the Student Debt Relief application has not been posted at the time of the writing of this update, we expect more details to be released over the coming days about the application process, which is expected to run from October 2022 through December 2023.

Who’s eligible

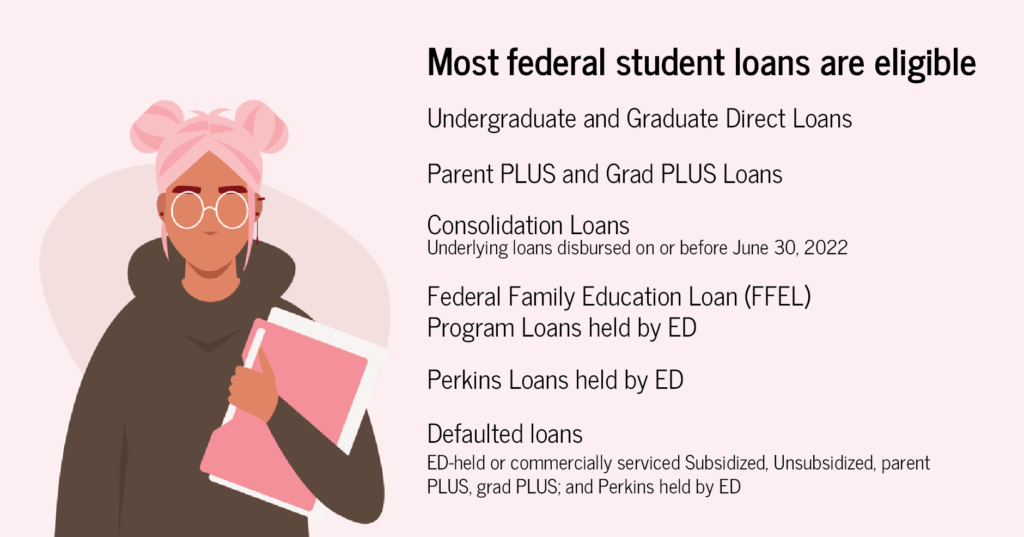

You are eligible if you have most federal loans (including Direct Loans and other loans held by the U.S. Department of Education) and your income for 2020 or 2021 is either:

- Less than $125,000 for individuals

- Less than $250,000 for households

If you are a dependent student, your eligibility is based on your parental income.

What you might be eligible for

- Up to $20,000 in debt relief if you received a Pell Grant in college

- Up to $10,000 in debt relief if you didn’t receive a Pell Grant

Insight #1: Your relief is capped at the amount of your outstanding debt. For example, if you are eligible for $20,000 in debt relief, but have a balance of $15,000 remaining, you will only receive $15,000 in relief.

How it’ll work

- Sometimes in October, for borrowers whose income data it doesn’t have, the U.S. Department of Education will launch a short online application for student debt relief. You won’t need to upload any supporting documents or use your FSA ID to submit your application.

Insight #2: Nearly 8 million borrowers may be eligible to receive relief without applying—unless they choose to opt out—because relevant income data is already available to the U.S. Department of Education.

- Once submitted, your application will be reviewed to determine your eligibility for debt relief by your loan servicer(s) to process your relief.

Insight #3: Borrowers are advised to apply by mid-November in order to receive relief before the payment pause expires on December 31, 2022. Most borrowers who apply can expect relief within six weeks.

Important Changes to the Student Loan System

The Student Debt Relief Plan also includes several rule changes to create a new income-driven repayment plan that is aimed at substantially reducing future monthly payments for eligible borrowers.

The changes would:

- Require borrowers to pay no more than 5% of their discretionary income monthly on undergraduate loans.

Insight #4: This is down from the 10% available under the most recent income-driven repayment plan.

- Raise the amount of income that is considered non-discretionary income and therefore is protected from repayment.

Insight #5: This rule change guarantees that no borrower earning under 225% of the federal poverty level—about the annual equivalent of a $15 minimum wage for a single borrower—will have to make a monthly payment.

- Forgive loan balances after 10 years of payments.

Insight #6: This is lowered from the previous 20 years, but applies only for borrowers with loan balances of $12,000 or less.

- Cover the borrower’s unpaid monthly interest.

Insight #7: This is a significant change because, unlike other existing income-driven repayment plans, no borrower’s loan balance will grow as long as they make their monthly payments—even when that monthly payment is $0 because their income is low.